Collyer Bridge

By Dylan Patel — February 21, 2024

Source: https://semianalysis.com/2024/02/21/groq-inference-tokenomics-speed-but/

Hello,

In my second week working with FundaAI, we have published a note on TPUs, now Funda’s most read work on Substack.

I have noticed the views there echoed in a few other places, like this academic paper:

"The dominant constraints on AI systems are shifting from raw compute capability to data movement, connectivity, energy efficiency, system-level integration, and cost effectiveness (e.g., $/token)."

"Connectivity is as critical as computation: Performance scaling increasingly depends on interconnect bandwidth, latency, and topology, requiring connectivity–compute co-design rather than treating networking as a secondary concern."

Fabian also made a similar comment on this back in December:

For years the semiconductor industry measured progress in FLOPs. More compute, faster chips, bigger clusters. That framing is now incomplete. The real constraint in modern AI infrastructure is not how fast individual GPUs compute. It is how fast thousands of them can share data with each other.

Kioxia: YMTC has three factories on the way that will more than double production (RT)

Funda also published a piece on Kioxia last week.

Kioxia has reportedly started operations at the second Kitakami building (K2) in September 2025, installing equipment and expanding cleanroom areas to further boost production.

We’ll be looking out for what they have to say about capital returns on their investor briefing in June.

Sentiment has recently been weighed down by reports of YMTC’s expansion plans:

-

Expansion: Each of the three new plants will produce 100,000 wafers per month.

-

Current Capacity: YMTC currently produces a combined 200,000 wafers per month from its first two fabs.

-

Self-Sufficiency: Over 50% of the equipment for the third factory (Wuhan) is sourced from domestic Chinese companies. The third factory has been completed and is currently installing equipment.

-

DRAM Entry: YMTC is also pivoting into DRAM; all three new plants will allocate some capacity to memory chips. The exact amount will depend on the company’s progress in developing those chips.

Another Chinese article continued to weigh on the stock today:

“Yangtze Memory Technologies Co., Ltd.’s revenue in the first quarter of this year exceeded 20 billion yuan, more than doubling year-on-year. Its NAND (flash memory) chip production has exceeded 10% of the global market share, approaching the third largest in the world,” said a core person in the memory chip industry chain. “The profits will be even more explosive in the future.”

Chinese imports of US chip tools from Singapore and Malaysia hit record (Nikkei Asia)

According to Nikkei Asia, Chinese imports of US chip tools from Singapore and Malaysia in 2025 have hit record highs.

-

Singapore: $5.7 billion (up 17% YoY).

-

Malaysia: $3.4 billion (more than double the 2024 figure).

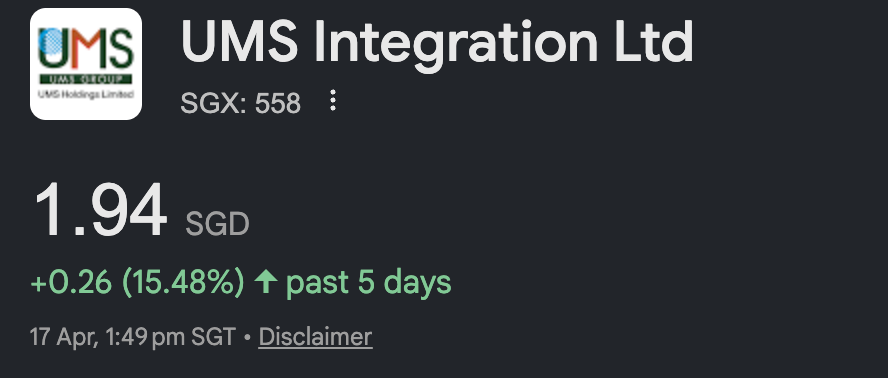

Lam Research is significantly expanding its manufacturing footprint in Malaysia. We believe UMS Integration’s facility (serving Lam) is currently at 50% utilization. The stock gained roughly 15% this week.

Some good news for Lam and Tokyo Electron too in the revised MATCH bill reported by Reuters here.

Hansol Group makes a small acquisition to enter the DRAM probe card market

Hansol is acquiring an 83.37% stake in Will Technology for ₩177.2 billion KRW (~US$120.6 million), implying a total valuation of US$144.6 million.

-

Will Technology is the #1 provider of probe cards for Samsung’s Galaxy S series APs and CIS (image sensor chips).

-

Hansol plans to use this acquisition to enter the DRAM probe card market and expand into China.

-

Valuation: We estimate this implies a P/E of ~24.4x and a P/S of ~3.15x. This might be seen as a rich valuation for a new entrant compared to established Japanese peers like JEM (6855).

Special thanks to one of our readers for flagging this.

Macronix thesis playing out elsewhere in Taiwan

In brief, the Macronix (2337.TW) thesis is that it is emerging as a highly profitable monopoly in the eMMC memory market as the "Big Four" memory giants abandon this market and reallocate their capacity toward high-margin HBM and high-end NAND flash.

There appears to be a similar play in another industry:

Zephyr@zephyr_z9

Basically, the DDR4 and legacy NAND situation is repeating with E-glass "E-glass thin fabrics have cumulatively risen 30% in 2025, with expectations of more than doubling in 2026. This data runs counter to intuition—the fiercest increases are in mid- to low-end fabrics. AI isn't

Macro_Lin|市场观察员 @LinQingV

市场把最近的 CCL 涨价潮普遍解读为”AI 需求景气、产业链向好”。这个解读漏掉了真正在驱动这轮涨价的两个供给端事件,而它们决定了涨价不是一两个季度的事情。 第一个事件是 SABIC 沙特 PPO 工厂停产。SABIC 占全球 PPO 份额七成,沙特工厂因天然气问题影响 25–30%

11:42 AM · Apr 15, 2026 · 4.32K Views

2 Reposts · 33 Likes

Fulltech makes an upstream material for the PCB/CCL supply chain: fiberglass yarn and woven cloth used as structural reinforcement in rigid CCL. Every rigid CCL sheet — produced by makers like Elite Material, ITEQ, and TUC — uses fiberglass cloth as its core reinforcement layer. Higher layer-count AI server PCBs consume proportionally more cloth, and IC substrates for AI accelerators require more advanced low-Dk or low-CTE grades, where supply is tightest and margins are highest.

A summary thesis has been posted on X and now has >100k views:

駿HaYaO@QQ_Timmy

#市場小作文 #RUMOR 轉 1815 富喬 1. 富喬營收組成為E-glass 30-40%/LDK 60-70%。 2. Nittobo戰略退出,E-glass超薄布出現「結構性缺口」:根據產業調研指出,全球玻纖布技術龍頭日東紡(Nittobo)正在逐漸退出E-glass市場,轉而專注於更高階的特殊玻璃(LDK/T-glass)。 -

7:13 PM · Apr 11, 2026 · 107K Views

3 Replies · 9 Reposts · 161 Likes

Fulltech's revenue mix is approximately 30–40% E-glass and 60–70% low-Dk.

Nittobo's strategic exit creates a "structural gap" in E-glass ultra-thin fabric: According to industry research, global fiberglass fabric technology leader Nittobo is gradually exiting the E-glass market to focus on higher-end specialty glass (LDK/T-glass).

As Nittobo exits the high-end ultra-thin fabric segment of E-glass, Fulltech, with its long-term deep cultivation in "ultra-thin fabric" products, is poised to fill the capacity gap in high-end E-glass production.

Benefiting from NV switch and Google TPU specification upgrades, it is expected that in 2H26, the supply and demand for E-glass/LDK 1/2 fiberglass fabrics will be severely imbalanced (estimated that Taiwan Optical Electronics' 2H26 LDK2 supply gap will reach 2 million meters/month+), and the price increases for E-glass/LDK will significantly expand.

In addition to new customer orders for LDK2, T-glass products have also passed overseas customer certification in 4Q25 (Low CTE strand for Japanese fabric factories, Low CTE fabric for Taiwan CCL factories), targeting a 10% revenue share for T-glass in 2026.

Conservatively estimated EPS for 2026/2027 is NT$6-8/~NT$10, with current valuation undervalued.

Another play on this idea is Unitika:

However, I have not gotten very good feedback on Unitika from sources close to the supply chain. It has been an excellent trade though!