GlobalFoundries Stuffing Customers With High Inventory – Underweight $GFS

By Dylan Patel — August 12, 2022

Source: https://semianalysis.com/2022/08/12/globalfoundries-stuffing-customers/

GlobalFoundries recently had their capital markets date, so we want to share our take on it. While the sell-side bankers are incredibly bullish, and the stock has gone up 20% over this week, we want to share our bearish view. We have even owned and recommended GlobalFoundries, but we are now a seller. As a side note, we have written extensively about them in the past, including capacity, expansion, and technology. We have said they are leading edge in specialty technologies, and in particular, we have praised their RF-SOI and silicon photonics “Fotonix” offerings. Our content was even included as a slide in the CTO’s capital markets day presentation this week.

Today we want to talk about how they are stuffing their customers with inventory, why their long-term commitments aren’t as rosy as they proclaim, why the geopolitical valuation argument holds very little water, and why we are negative on the firm’s stock.

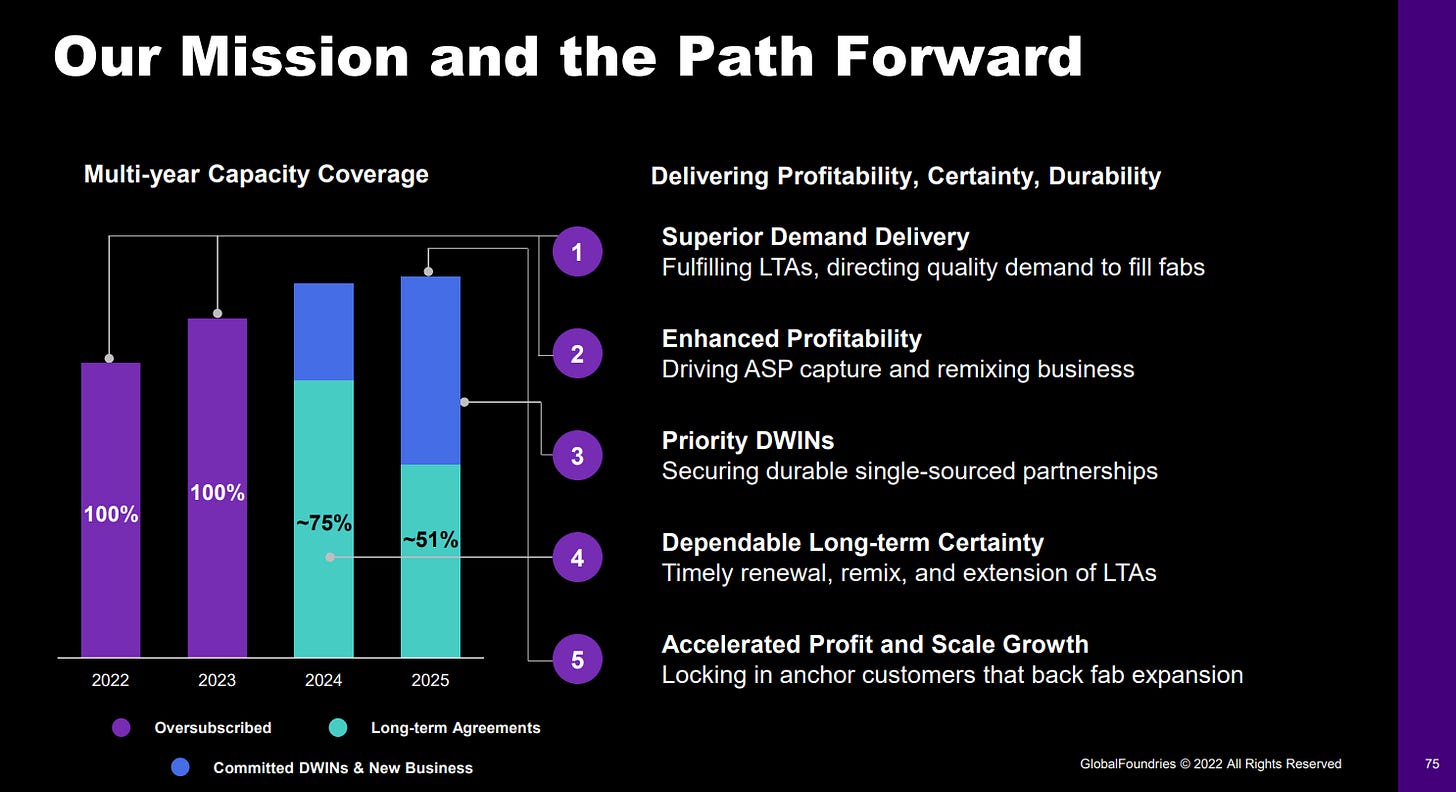

First, a bit of context, their margins are expanding, and their utilization rates are excellent. They are fully booked for the next few years.

Everything seems fantastic right?

Not in our opinion.

GlobalFoundries customers are doing badly. While they champion some of their growth vectors and long-term agreements, the customers feel the pain. GlobalFoundries is very smartphone exposed even if they try to say they are not. Our estimates have them as more smartphone exposed than even TSMC.

If you don’t believe our calculations, here’s a list of their biggest customers with long-term agreements.

Qualcomm, MediaTek, NXP, Qorvo, Cirrus Logic, AMD, Skyworks, Murata, Samsung, and Broadcom.

Look into the types of chips they are buying. Most of these customers are using GlobalFoundries for consumer smartphones, consumer IoT, or consumer PC.

Qorvo, in particular, has been very open about their troubles. While they didn’t say it, we can confirm the foundry. It is GlobalFoundries

The $110 million is the amount of a particular agreement that we feel we couldn't live up to according to the existing terms, which we're negotiating now with the supplier.

Q1 2023 Earnings Call – August 3rd, 2022

They took a charge because they couldn’t meet the minimum purchase requirements, and now they are negotiating. They already know GlobalFoundries is a tough negotiator.

GlobalFoundries’ biggest customer, Qualcomm, is having issues as well. You may disagree because of the recent PR they put out about a long-term agreement through 2028, but it was actually negative in our opinion.

This requires some historical context about the AMD and GlobalFoundries. They had a long-standing agreement, WSA (Wafer Supply Agreement). AMD fell short of volumes throughout the 2010s. Rather than letting their struggling partner cut back on volume, they charged them penalties multiple times and even demanded prepayments. AMD had a very tough time even being allowed to use TSMC 7nm. For a period of time, they had to pay GlobalFoundries for every external wafer utilized. Now the WSA is a favorable agreement that helps them lower costs, but previously it was not.

We believe the same is happening today with Qualcomm and GlobalFoundries. Qualcomm thinks they can’t meet their minimum purchase requirements despite winning a huge share in automotive RF, RFFE, and even 100% of Samsung premium smartphones for the next year or two.

Qualcomm is likely to renegotiate its supply agreement, which involved signing a contract for more than 5 years, to temper the impact of the oversupply in smartphones over the next 1.5 years.

The same will happen to all of GlobalFoundries clients who are consumer-exposed. Sure, they won’t be able to cut orders as they would like, and GlobalFoundries will have near full utilization over the next couple of years, but their clients will either be stuffed with inventories or negotiate for lower but longer purchase agreements. This isn’t good for the long-term trust of fabless companies in GlobalFoundries. This also comes as TSMC invests heavily into winning back RF-SOI share

The geopolitical argument holds no water. As we explained in “I, Semiconductor – The Regionalization Of Semiconductors Due To Global Supply Chain Instability”, GlobalFoundries is not geopolitically diverse. More than half their production is in Singapore.

Is Singapore any more secure than Japan or South Korea?

We think not. Even Samsung and SK Hynix are more geopolitically secure, in our opinion. Samsung and SK Hynix work with China and the US in a way that makes them the biggest beneficiary of a US-China divided world with the potential Taiwan invasion. Samsung, in particular, has a higher share in foundry and is the only foundry that currently competes with TSMC on 7nm and below. The TAM for that market is way more significant than the specialty technologies that GlobalFoundries is pushing. Intel is trying, but we need to see wafer agreements to believe that story, not empty PR.

With that said, we don’t think Samsung is a good investment either, given their cultural issues and where the DRAM market and NAND market are headed.

GlobalFoundries might be a stupid short, but it’s definitely not a buy.

Pay attention to the float. It’s incredibly low. Mubadala would love to offload more, but the IPO intentionally kept it very low float because they knew they couldn’t offload much more. The public market holders are pretty long-term oriented too. So a few sellers or buyers can swing the price quite a bit.

Mubadala will offload more at some point and the stock will go down, so they will be slow and tepid about that.